All Categories

Featured

Table of Contents

Life insurance isn’t just a policy; it’s a powerful way to secure your family’s financial stability. From protecting your loved ones from unexpected costs to planning for the future, the right life insurance policy ensures peace of mind. Term life insurance is a popular choice for those seeking temporary, cost-effective coverage, while whole life insurance provides lifelong protection and cash value growth. Universal life insurance is another flexible option, ideal for families and individuals looking to balance affordability with long-term financial goals.

For specific needs, final expense insurance ensures funeral costs are covered, and mortgage protection life insurance provides reassurance that your family can stay in their home. Accidental death insurance adds another layer of security for unique situations (instant life insurance quotes from an agent). Many of these policies also include living benefits, allowing policyholders to access funds during critical times, such as illness or emergencies

Life insurance isn’t just about protecting your loved ones; it’s also a strategic tool for building a solid financial foundation. Speak with a licensed insurance agent today to explore policies designed for your specific needs, whether you’re planning for retirement, saving for college, or securing your family’s future. Request a free quote now to start building a secure tomorrow.

They typically provide an amount of insurance coverage for a lot less than long-term kinds of life insurance policy. Like any type of policy, term life insurance has benefits and downsides relying on what will certainly function best for you. The benefits of term life consist of price and the capability to personalize your term size and protection quantity based on your demands.

Depending upon the sort of policy, term life can provide fixed premiums for the entire term or life insurance policy on degree terms. The survivor benefit can be fixed as well. Since it's an inexpensive life insurance policy item and the settlements can stay the exact same, term life insurance coverage policies are popular with youths simply starting, family members and people that want defense for a details period of time.

Reputable Term To 100 Life Insurance

Fees show policies in the Preferred And also Rate Course problems by American General 5 Stars My representative was really well-informed and handy in the procedure. July 13, 2023 5 Stars I was satisfied that all my needs were satisfied without delay and skillfully by all the agents I spoke to.

All paperwork was digitally finished with access to downloading for personal documents upkeep. June 19, 2023 The endorsements/testimonials offered must not be taken as a referral to purchase, or an indication of the worth of any type of services or product. The testimonies are real Corebridge Direct consumers that are not associated with Corebridge Direct and were not given settlement.

2 Cost of insurance policy rates are identified using approaches that vary by firm. It's important to look at all aspects when examining the overall competitiveness of prices and the value of life insurance coverage.

Reputable Level Term Life Insurance Meaning

Like many group insurance plans, insurance coverage plans provided by MetLife have specific exemptions, exemptions, waiting durations, reductions, constraints and terms for keeping them in pressure (joint term life insurance). Please contact your advantages manager or MetLife for prices and full information.

For the a lot of component, there are 2 types of life insurance policy plans - either term or long-term plans or some combination of the two. Life insurers supply various kinds of term strategies and conventional life plans as well as "passion delicate" items which have come to be more common since the 1980's.

Term insurance coverage supplies security for a given duration of time. This period might be as brief as one year or give coverage for a particular variety of years such as 5, 10, two decades or to a specified age such as 80 or in some cases up to the earliest age in the life insurance policy mortality.

Premium Does Term Life Insurance Cover Accidental Death

Presently term insurance prices are very competitive and among the most affordable historically knowledgeable. It should be kept in mind that it is an extensively held idea that term insurance policy is the least pricey pure life insurance protection readily available. One needs to assess the plan terms thoroughly to choose which term life choices appropriate to satisfy your particular situations.

With each brand-new term the costs is raised. The right to restore the policy without evidence of insurability is a crucial benefit to you. Otherwise, the danger you take is that your wellness may weaken and you may be incapable to acquire a plan at the same rates or perhaps whatsoever, leaving you and your beneficiaries without insurance coverage.

The size of the conversion duration will differ depending on the type of term policy acquired. The premium rate you pay on conversion is typically based on your "present obtained age", which is your age on the conversion date.

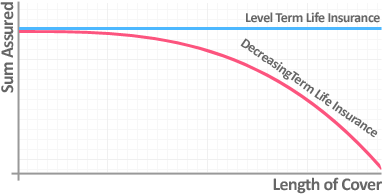

Under a level term plan the face amount of the plan continues to be the exact same for the whole period. Frequently such plans are sold as home mortgage protection with the amount of insurance reducing as the equilibrium of the home mortgage lowers.

Commonly, insurance companies have actually not had the right to change costs after the plan is marketed (level term life insurance definition). Since such policies may proceed for years, insurance companies have to use conventional mortality, rate of interest and expenditure price quotes in the premium computation. Adjustable premium insurance, nonetheless, enables insurers to use insurance at lower "existing" costs based upon much less conventional presumptions with the right to change these costs in the future

Guaranteed Does Term Life Insurance Cover Accidental Death

While term insurance coverage is developed to supply protection for a defined period, irreversible insurance is made to offer coverage for your entire life time. To maintain the premium price level, the costs at the more youthful ages surpasses the actual price of protection. This additional premium builds a book (money value) which aids spend for the policy in later years as the price of security surges over the premium.

The insurance policy business invests the excess costs dollars This type of policy, which is occasionally called money value life insurance policy, generates a savings element. Money values are vital to an irreversible life insurance coverage plan.

Effective Decreasing Term Life Insurance

Often, there is no relationship between the dimension of the money worth and the costs paid. It is the money value of the plan that can be accessed while the policyholder lives. The Commissioners 1980 Requirement Ordinary Death Table (CSO) is the existing table used in determining minimal nonforfeiture worths and plan books for normal life insurance policy plans.

Several irreversible policies will consist of stipulations, which specify these tax obligation requirements. There are 2 fundamental categories of long-term insurance policy, typical and interest-sensitive, each with a number of variations. Additionally, each group is typically available in either fixed-dollar or variable form. Standard whole life policies are based upon long-lasting quotes of cost, interest and death.

If these quotes transform in later years, the business will certainly readjust the premium as necessary but never ever over the optimum ensured costs mentioned in the policy. An economatic entire life policy offers a standard quantity of participating entire life insurance policy with an added supplemental coverage given via the usage of dividends.

Because the premiums are paid over a much shorter span of time, the premium repayments will be more than under the entire life plan. Single premium entire life is limited repayment life where one large premium payment is made. The policy is completely compensated and no additional costs are called for.

{kind=link}

Table of Contents

Latest Posts

The Best Funeral Policy

Best Funeral Plan For Over 50

Funeral Insurance Brokers

More

Latest Posts

The Best Funeral Policy

Best Funeral Plan For Over 50

Funeral Insurance Brokers